You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Cointegration-/Pairs-Trading

- Thread starter TopFroxx

- Start date

- Status

- Not open for further replies.

allocation changed a bit.

uj still the biggest position, but e/g long and g/chf short aggregated (eg long and gchf short pretty much the same thing) are of the same size as the uj long now. wont be changing the scaling factor anytime soon, unless i have a clear bias on uj AND eg. so will probably be sticking to 0.9 for the time being.

uj still the biggest position, but e/g long and g/chf short aggregated (eg long and gchf short pretty much the same thing) are of the same size as the uj long now. wont be changing the scaling factor anytime soon, unless i have a clear bias on uj AND eg. so will probably be sticking to 0.9 for the time being.

TopFroxx said:allocation changed a bit.

uj still the biggest position, but e/g long and g/chf short aggregated (eg long and gchf short pretty much the same thing) are of the same size as the uj long now. wont be changing the scaling factor anytime soon, unless i have a clear bias on uj AND eg. so will probably be sticking to 0.9 for the time being.

well, so much for the plans. just scaled up to 1. uj at 102.80, looks to me like we will see 103.30 at least. and if it's only one stab to collect liquidity prior to todays fomc statement. 103.10 and 103.30 clean levels and perfect targets.

at the same time eg sitting at 0.84 support level. gu just did some liquidity collecting, fiber still likely to tag 1.38 imo. all with the the premise of a bigger move or at least some volatility given todays fomc statement. fiber also currently sitting at a good level for long, although for a manual entry i would wait for a stab down to 40ish and then a strong rejection of 15 pip or so within very short time. 1.tp would be 1.3780.

sorry for mixing in some possible manual trading setup, but if fiber is likely to make a move up, there is increased probability that eg will do as well in this setting.

I agree on the manual intervention.. with something like FMOC / QE Tapering announcements as a disruptor, I'd want to reduce my directional exposure on USD and 'risk on / risk off' sensitive currencies.

Enjoying your journal so far. Just wish there was some way to better visualize the basket as you update.

")

Enjoying your journal so far. Just wish there was some way to better visualize the basket as you update.

Jack said:Enjoying your journal so far. Just wish there was some way to better visualize the basket as you update.

thanks. could you elaborate or do you have an idea/suggestion how to visualize?

edit: could do something like this, dont know if that helps. exposure in euro per currency.

would need to write a macro for a daily update in this form though, but i could do that if you are interested.

Attachments

I was thinking more like a way to visualize the weighting's change over time and how that compares to the account's unrealized+net % return.

So that way we can see the rate of change (in weightings), and the impact on returns it has (if any) between periods.

Perhaps a bar chart with bar's being divided up by weightings and an overlay line graph of % unrealized+net (and by that I mean % returns including floating positions.)

(EDIT: this would be something that's cumulative, so the chart would get more and more interesting as new periods are added and we can see it grow.)

I know that's asking a lot.. so unless that sort of thing is easy for you to automate and generate, don't worry too much about it. I just like making visuals of relationships between datasets. ;P

EDIT2: Also, if you're worried about copy-traders.. you can always just put a significant time delay between adjustments in your positions and posting it here.

So that way we can see the rate of change (in weightings), and the impact on returns it has (if any) between periods.

Perhaps a bar chart with bar's being divided up by weightings and an overlay line graph of % unrealized+net (and by that I mean % returns including floating positions.)

(EDIT: this would be something that's cumulative, so the chart would get more and more interesting as new periods are added and we can see it grow.)

I know that's asking a lot.. so unless that sort of thing is easy for you to automate and generate, don't worry too much about it. I just like making visuals of relationships between datasets. ;P

EDIT2: Also, if you're worried about copy-traders.. you can always just put a significant time delay between adjustments in your positions and posting it here.

think i understand what you mean. i could do this historically with floating return from myfxbook (i think it is possible to download data from myfxbook, isnt it?) and with the historical positions from matlab. what i cant do is show the impact of my manual scaling, because i dont have that saved for the whole period. i'll have a look and will try to create a historical graph for my forward testing period later today

well, sucks that the eg position got increased in the last days. dropped like a stone. uj on the other hand did a good job (again) and paired the losses from eg. overall a moderate positive day.

also just did the calculations for today. eg long positions more than halfed, generally much less gbp short. so realized some losses from those positions today. uj long again about 70% of the portfolio.

also just did the calculations for today. eg long positions more than halfed, generally much less gbp short. so realized some losses from those positions today. uj long again about 70% of the portfolio.

hey all,

hope everyone had a nice christmas. just thought i'd briefly recap the live performance so far.

overall i am positively surprised. the forward performance is quite a bit above the average performance during the backtesting period. on the other hand, historically there were also some periods (of a few months) that went really well, so this currently is probably just an extremely well suited environment for the strategy. this leads to the fact that i was long UJ during the whole period (sometimes more, sometimes less, but always long). this was definitely the main driver of the overall performance and the day will come when UJ isnt going to climb anymore. that will be the ultimate forward test for this strategy. how will it handle a bigger top in uj? historically it also performed well during major UJ downtrends, but let's see if it manages to identify the top in a timely fashion.

attached you find the equity growth chart, a little less than 3 months in. it would be foolish to believe it will continue like this though (especially without larger drawdowns).

also, i am not going to leave the strategy exactly like this. i have tinkered with it again and again so the performance also reflects the process, it's not a fixed system. and every time i have a new idea and i find the time i will implement it and see if it helps. the next thing i will look at will be the dependency of the performance on the yen pairs. after identifying the relationship i will try to develop and implement a suited risk management measure to further stabilize portfolio performance without lessen the returns too much. i already looked a bit at portfolio allocation and performance and the times where risk is concentrated on 2 or 3 currencies (e.g. JPY and USD) are also the most profitable times. so it's not going to be easy.

ok, that's it from me for now. happy new year everyone and a profitable year 2014!

hope everyone had a nice christmas. just thought i'd briefly recap the live performance so far.

overall i am positively surprised. the forward performance is quite a bit above the average performance during the backtesting period. on the other hand, historically there were also some periods (of a few months) that went really well, so this currently is probably just an extremely well suited environment for the strategy. this leads to the fact that i was long UJ during the whole period (sometimes more, sometimes less, but always long). this was definitely the main driver of the overall performance and the day will come when UJ isnt going to climb anymore. that will be the ultimate forward test for this strategy. how will it handle a bigger top in uj? historically it also performed well during major UJ downtrends, but let's see if it manages to identify the top in a timely fashion.

attached you find the equity growth chart, a little less than 3 months in. it would be foolish to believe it will continue like this though (especially without larger drawdowns).

also, i am not going to leave the strategy exactly like this. i have tinkered with it again and again so the performance also reflects the process, it's not a fixed system. and every time i have a new idea and i find the time i will implement it and see if it helps. the next thing i will look at will be the dependency of the performance on the yen pairs. after identifying the relationship i will try to develop and implement a suited risk management measure to further stabilize portfolio performance without lessen the returns too much. i already looked a bit at portfolio allocation and performance and the times where risk is concentrated on 2 or 3 currencies (e.g. JPY and USD) are also the most profitable times. so it's not going to be easy.

ok, that's it from me for now. happy new year everyone and a profitable year 2014!

Attachments

wow, it happened. at least to some extent. after the most recent calculations all yen long position got decreased quite a bit. UJ long now only makes for 30% of the overall portfolio, which is an all time low in the forward testing period.

biggest position now is e/g long and g/chf short. e/g dropped quite a bit and the strategy seems to expect a recovery. i am not too sure about that one. i am not going to tinker with it at the moment and leave the scaling factor at 1. could see a further drop to 0.8220 in my opinion, which is where i would start to look at a possible increase in positions. if price rises on the other hand, i will scale back a bit (to 0.9) at the close of the weekend/holiday gap around 0.8308.

biggest position now is e/g long and g/chf short. e/g dropped quite a bit and the strategy seems to expect a recovery. i am not too sure about that one. i am not going to tinker with it at the moment and leave the scaling factor at 1. could see a further drop to 0.8220 in my opinion, which is where i would start to look at a possible increase in positions. if price rises on the other hand, i will scale back a bit (to 0.9) at the close of the weekend/holiday gap around 0.8308.

"USDJPY Slumps Most In 4 Months As Nikkei Futures Tumble 450 Points"

wow, i have to say, i'm impressed. still sitting on an 8% drawdown currently (combined mainly from eg long and uj long), but it could have been quite a bit worse.

no changes in portfolio allocation currently.

wow, i have to say, i'm impressed. still sitting on an 8% drawdown currently (combined mainly from eg long and uj long), but it could have been quite a bit worse.

no changes in portfolio allocation currently.

TopFroxx said:"USDJPY Slumps Most In 4 Months As Nikkei Futures Tumble 450 Points"

wow, i have to say, i'm impressed. still sitting on an 8% drawdown currently (combined mainly from eg long and uj long), but it could have been quite a bit worse.

no changes in portfolio allocation currently.

To think, the cash equity market in Japan has been on holiday for the last few days as well.. so this slump and move has been without their local exchanges moving shares.. This coming Monday they'll be opened back up and we'll see the fallout in the cash equity market (and anyone who wanted to sell but couldn't can get their chance..)

Jack said:To think, the cash equity market in Japan has been on holiday for the last few days as well.. so this slump and move has been without their local exchanges moving shares.. This coming Monday they'll be opened back up and we'll see the fallout in the cash equity market (and anyone who wanted to sell but couldn't can get their chance..)

at the end of today the strategy better tells me to short then

TopFroxx said:wow, it happened. at least to some extent. after the most recent calculations all yen long position got decreased quite a bit. UJ long now only makes for 30% of the overall portfolio, which is an all time low in the forward testing period.

biggest position now is e/g long and g/chf short. e/g dropped quite a bit and the strategy seems to expect a recovery. i am not too sure about that one. i am not going to tinker with it at the moment and leave the scaling factor at 1. could see a further drop to 0.8220 in my opinion, which is where i would start to look at a possible increase in positions. if price rises on the other hand, i will scale back a bit (to 0.9) at the close of the weekend/holiday gap around 0.8308.

eg almost reached that noted 0.8220 level. increased to 1.15 at 0.8235. looking for 0.8275 to scale back to 1.1

with the slumps in eg and also uj my drawdown went up to 14% a couple of days ago. but like it historically has always done, rebounding quite nicely the last 2 days or so. every sharp drop in equity is followed by an at least equally sharp or even "sharper" increase in equity. thats a "pattern" that i also adjusted my money management to with this strategy. (edit to clarify: this is about the steepness, also about the return, but mainly about with how much force and how fast it rebounds)

currently still sitting at a drawdown of 7% from the high, but still well in the green with 33% over the last 3 months.

allocation: general structure hasnt changed much, but uj long again has become the largest position over the past days. uj long and eg long make for about 75% of the portfolio, both contributing about equal.

a bit off topic: i'm thinking about another thread for another "quant" strategy. it's a bit more simple, just based on patterns of daily candles on EU. historically evualted the probability and profitability of a lot of patterns. if anyone is interested, let me know. dont know if it is worth it (not sure if anyone is reading this thread [it's quite boring, i got to admit], so there might be no point in starting another, similar one).

currently still sitting at a drawdown of 7% from the high, but still well in the green with 33% over the last 3 months.

allocation: general structure hasnt changed much, but uj long again has become the largest position over the past days. uj long and eg long make for about 75% of the portfolio, both contributing about equal.

a bit off topic: i'm thinking about another thread for another "quant" strategy. it's a bit more simple, just based on patterns of daily candles on EU. historically evualted the probability and profitability of a lot of patterns. if anyone is interested, let me know. dont know if it is worth it (not sure if anyone is reading this thread [it's quite boring, i got to admit], so there might be no point in starting another, similar one).

Jack said:I was thinking more like a way to visualize the weighting's change over time and how that compares to the account's unrealized+net % return.

So that way we can see the rate of change (in weightings), and the impact on returns it has (if any) between periods.

Perhaps a bar chart with bar's being divided up by weightings and an overlay line graph of % unrealized+net (and by that I mean % returns including floating positions.)

(EDIT: this would be something that's cumulative, so the chart would get more and more interesting as new periods are added and we can see it grow.)

I know that's asking a lot.. so unless that sort of thing is easy for you to automate and generate, don't worry too much about it. I just like making visuals of relationships between datasets. ;P

EDIT2: Also, if you're worried about copy-traders.. you can always just put a significant time delay between adjustments in your positions and posting it here.

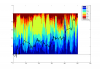

btw i didnt forget about this. i tried but could not find any significant pattern comparing relative currency positions vs equity. maybe it's neccessary to adjust the relative positions with the historical performance of that currency in some way.

but maybe i am just blind. attached you find the aggregated realtive positions for each currency. they are realtive to the overall portfolio, so they all add up to 1. the black line is the scaled equity curve. historical performance over the past ~2 years. if anyone can find a pattern in there that i cant see, please let me know

Attachments

TopFroxx said:a bit off topic: i'm thinking about another thread for another "quant" strategy. it's a bit more simple, just based on patterns of daily candles on EU. historically evualted the probability and profitability of a lot of patterns. if anyone is interested, let me know. dont know if it is worth it (not sure if anyone is reading this thread [it's quite boring, i got to admit], so there might be no point in starting another, similar one).

Right now the majority of our members are lurkers, but that's the same with most forums. People are reading your journal (I am for instance.

) That said, the worst that could happen is you find the daily candle strategy doesn't work as you expected and you wrap up your journal... the best is it takes off and a bunch of people start asking questions and following along. So do feel free to start another thread if you wish.

- Status

- Not open for further replies.